Storytel is a Swedish book streaming service which consists of two divisions, Streaming and Print Publishing. STORY is currently operating in 11 countries and the company is expanding heavily. The business has a large economic moat because the company buys up local publishers and then record all their books into audiobooks in the local language and make them available to their subscribers on their service. Buying the publishers makes it significantly harder for competitors to launch a similar product in the countries that Storytel operates in as competitors will not be able to get the rights to the content.

As Storytel was very early in the book streaming business they already have a strong foothold on European markets shown by their dominant market share (80% for example in the Netherlands) and that with the exception of India, Amazon's Audible is yet to launch in a single country where Storytel is operating.

The book publishing industry has had 0 to negative growth for years and therefore the publishing companies can be bought at attractive prices and then be used in the highly profitable streaming business. These companies are often very positive to get a new owner which can help them be a part of the direction the industry is taking. This makes acquisitions very attractive for Storytel as they can own the content itself and that the steady revenue from Print Publishing can be used to fund further growth and to cover expenses of entering new markets. The company has a gross margin of 38% and is at the moment not profitable as it is using money to expand itself on new markets such as Poland, Russia and Spain and entering new countries such as India, UAE, Mexico and Bulgaria. The biggest competitor is Audible, Amazon's streaming service but they aren't really competitors as they operate in different countries and in different languages. Storytel also have several competitors in the Nordic markets but Storytel has a majority of the market share. Unlike streaming movies, books are almost exclusively listened to in one's mother tongue and Audible mainly records English audiobooks and they also don't own the content themselves. Storytel owns several publishers and by owning the content that is created they can build an economic moat around their business that restricts competition as content consumed in a certain country is generally only in the local language.

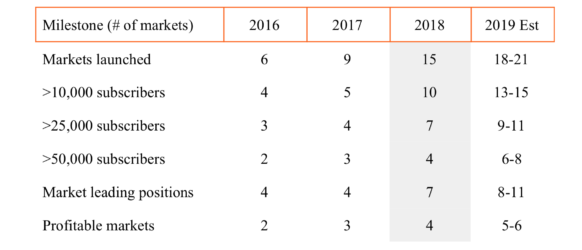

This picture showcases the number of markets the company is active in and their size. It is worth noting that while it may look like the number of profitable markets is lagging behind this is because it takes a bit of time for a market to reach profitability while it takes no time to launch a brand new market. It is noteworthy however that if the company was not establishing itself in new countries and in new markets it would in fact be turning a profit.

Current percentage of the population that pay for the service in Sweden is 4.5% and in Denmark and Norway about 2-3%. Kepler Cheuvreux predicts that the market penetration for digital audiobooks in highly technological countries will be about 5-10% of the population and in other countries about 2-3%.

In the process of making a valuation of the company it can be compared to fellow streaming companies Netflix and Spotify. Comparing Netflix to Storytel is especially relevant as both companies own a large share of the content that is available on their platforms. Metrics such as EV/EBIT and Price to Earnings that are used in valuations cannot be applied in this case since Storytel and Netflix do not turn a profit. Metrics such as EV/R and gross profit are in this case more relevant.

EV/R (Enterprise Value/Revenue)

Storytel 3.5

Netflix 10.2

Spotify 4.5

Market cap/Gross Profit

Storytel 8

Netflix 26

Spotify 20

Gross Margin

Storytel 40%

Netflix 35%

Spotify 24%

P/S (Price/Sales)

Storytel 3.9

Netflix 9.5

Spotify 4.4

P/B (Price/Book Value)

Storytel 10.5

Netflix 28

Spotify 14

As seen above according to these metrics Storytel has a lower valuation than some of its streaming counterparts. This valuation is lower then it should be as it fails to consider the moats of the business and the growth potential. It is my belief that the stock is misunderstood and considering future revenue and coming expansions into new markets the stock is undervalued.

Storytel recently did a directed equity issue of 55 million dollars for further expansion. This only makes the stock more attractive since further capital will be able to speed up the process of launching new markets and making them profitable. Bringing in outside capital is also better for the company as it avoids taking on debt and could potentially get more experienced owners.

The company has also shown that is can expand into a wider section than just audiobooks when it bought the Swedish startup Ztory which allows readers for a fixed cost every month to gain access to many different magazines. By acquiring this company they can create an even more attractive offer as their customers are very likely to be interested in reading magazines as well as listening to audiobooks. They have also created an E-reader that can be used to read books as well as listen to them and considering the success Kindle has had this might be quite a lucrative product.

The stock has recently suffered a downturn even though revenue and number of subscriptions have been heavily increasing. However, management have themselves expressed their belief in the company and there have been transactions made by management and the board. The majority of upper management hold equity in the company which they themselves have bought on the open market. The company is led by it’s founder Mr Tellander who serves as CEO and he himself together with his wife owns 16,2% of the total equity in the company. The largest shareholder is a board member who owns 22,7% of the total equity.

In the EU, print books have a lower VAT tax than ebooks. A decision by the EU was recently made that every single country will now be able to themselves change the VAT tax for ebooks and audiobooks, encouraging countries to lower them to the same amount as print books. The current VAT tax in Sweden, which makes up slightly less than 50% of its revenue from streaming is 25% and support for a lowering of the VAT tax for ebooks in the Swedish parliament is strong. Lowering the VAT tax from 25% to the same as print books in Sweden(6%) would dramatically increase earnings. This also applies to many other countries in the EU that Storytel is operating in as they also plan to have a vote in parliament to lower the VAT tax on audiobooks.

Catalyst

Resolution of the tax issue could be a catalyst. Even though this event isn’t certain to cause a bump in the stock price the company has excellent fundamentals and it is according to me trading below its intrinsic value based on current revenue and future growth potential.

Disclaimer: I own stock in the company.

Disclaimer: I own stock in the company.

Very interesting case, especially during the COVID-19 pandemic with people staying home and listening to more books.

ReplyDelete