Kollect on Demand operates an online marketplace that connects customers (domestic and business) who need to dispose of waste with waste companies who collect it. The company operates in Ireland and was recently launched in the UK.

Disclaimer: I own stock in the company and I am most likely biased. Always do your own due diligence. This is not investment advice.

Summary

Two sided marketplace digitizing an offline industry

Long runway in a large market as only 0,5% of waste services are booked online

Founders with experience in waste management and technology that together own 51% of the company

Undiscovered nano cap trading at an attractive price with a revenue CAGR of 103% from 2016 - 2020.

61% recurring revenues with low customer churn

Steadily improving margins as the business scales

Reopening of Ireland and the UK will drive revenue in the commercial business segment

The waste management industry is an industry that has yet to undergo the transformation to digital. The company estimates that only 0,5% of waste activities are booked online. In comparison, 39 percent of travel was booked online in the U.S in 2016 and global e-commerce spending represents almost 15% of all consumer spending in 2020. The extremely low online penetration in the waste industry is explained by the fact that no online solution exists on the market. In order to buy waste management services, customers need to manually find different waste management companies and call around to get different price quotes. On Kollect’s website however, customers can easily buy any solution that suits their waste needs and it takes less than 60 seconds to book a waste collection service. Whereas traditional waste companies are only open from 9 to 5 during weekdays, Kollect’s platform is always online and customer service is open 7 days a week to 10 PM.

The second business area is the BIGbin which is a waste drop-off solution intended for domestic and commercial waste. The BIGBin offers an alternative to long-term waste contracts for collection. The bins are placed in locations such as garages, supermarkets, car parks and in apartment complexes. One large partner in this business area is Circle-K which recently renewed their contract with Kollect and chose to add 260 new potential sites for the BIGBin. As of 31 December 2020, the company has 31 sites in use. The BIGbins have excellent unit economics and have a 20 year life span resulting in steady, predictable cash flows.

Value proposition for waste management companies

As the company operates a two-sided marketplace, it is crucial that the company efficiently attracts and retains both waste contractors and consumers on the platform. So why would waste contractors want to use the platform at all? By partnering with Kollect, waste contractors gain access to more customers and are able to generate more sales. In addition to this, their customer acquisition and service costs on customers acquired through the platform is zero as Kollect provides them with customers and handles the support and service. Partnering with Kollect also provides the waste management companies with technology in their daily operations which makes their operations more efficient. Traditional waste companies have customers spread all across cities and therefore much time is spent driving back and forth for different assignments. Kollect uses route optimization software that instead assigns contractors tasks that are in their vicinity to maximize output. This results in less fuel being used by the trucks and that a single driver can complete more jobs per day as less time is spent driving around. By using Kollect, waste contractors maximize output which generates more sales and their operational costs are lowered with the help of technology.

A barrier to entry in the waste management industry is that in order to be competitive, you need to achieve economies of scale through volume. Waste operators pay fees to dispose of waste and by achieving scale, the fee costs per tonne can be lowered. In other words, the marginal cost of collection falls as the quantity of waste collected increases. Because of this, waste contractors want to increase their volumes and should therefore be inclined to partner with Kollect. Waste management is a very local, fragmented industry and it is estimated that 80% of waste management companies have under 10 employees in Ireland and in the UK. Kollect’s offering is very attractive to these companies as they are able to outsource activities that they have no expertise in, such as digital marketing, customer acquisition and technological development. Instead, they can focus on what they are really good at, which is waste collection.

To summarize, contractors partner with Kollect as they want to increase revenues, volumes and achieve economies of scale. In a more digitized environment where customers prefer to book services online, these companies will have to adapt in order to stay competitive. However, waste management companies neither have the knowledge, competence or resources to adapt to this change in customer preference themselves. To leverage the power of technology to their advantage, they will therefore turn to a platform like Kollect.

Value proposition for customers

Consumers are also huge beneficiaries of the solution that Kollect provides. Through a click of a button, they can handle all of their waste management needs in just a few minutes. The alternative to this is having to look for different contractors on dozens of different websites and call them to get a price quote. In addition to this, it is hard for customers to judge the quality of the services and know if contractors are licensed and vetted. Waste operators on Kollect’s platform however, are both licensed and vetted. Many customers are also environmentally conscious and Kollect appeals to them as the company focuses on sustainable waste disposal and makes sure that no waste goes to landfill.

Customers are also provided with a better service as the platform grows. As the supply of services increases, more waste contractors will compete for the same contracts. This will lead to faster service and lower prices for consumers. This will result in services and prices improvíng over time (up until a certain point). It is extremely hard for any single contractor to compete with this offering.

Kollect also offers services to commercial customers through their proprietary developed mobile app. The app offers several valuable functions such as statistics, reporting and new point of sale applications. Another function that Kollect offers to commercial customers is centralised billing. As an example, construction companies have dozens of building sites spread across Ireland which produce large amounts of waste. The waste collection needs to be coordinated at all these sites with various different, local contractors. Kollect can take care of this whole process and administer, coordinate, follow up and bill all the waste collection. Kollect can offer a one stop shop solution to all sorts of enterprises which creates immense value for them.

Online marketplaces are famous for having to tackle the “chicken-or-egg problem” but Kollect’s services have huge appeal and provide value for both sides of the transaction. This has led to them being able to attract both customers and waste companies to the platform.

Competitive advantages

An online marketplace such as Kollect has potential to build durable competitive advantages and strong economic moats.

As more customers join, more waste companies will want to access these customers and join the network. As the amount of waste contractors increases, so does competition resulting in a faster service and lower prices. This will in turn drive more customers to the platform. This virtuous cycle is what is known as a network effect. If similar marketplaces were to appear, customers would not be interested in switching as Kollect would have the lowest prices and fastest service. Contractors would also want to stay with Kollect as the platform would have such a large customer base.

I would also argue that the business has switching costs for the contractors. If waste companies partner with Kollect, a large portion of their business is handled through Kollect’s platform. Without Kollect, they do not have access to these customers as the transaction is handled through Kollect and if they were to leave the platform they would lose these customers. This could be a huge loss of revenue and therefore, there are significant switching costs and the platform can more or less lock in contractors. Switching costs could also be in the form that contractors are used to Kollect’s systems and therefore do not want to switch and learn new systems.

I believe that Kollect could create a competitive advantage through the brand that they are building. Waste management is a “boring” industry, delivering quite a standardized service and there are few to no real brands at all in the industry. Through branding, the company can create customer awareness and become the top of mind company for people looking to get rid of their waste. Kollect has a 4.8 rating on TrustPilot and the company is focused on “Wowing” their customers and continually adding value to their customers. This sets the company apart from competitors.

Historically, the waste management industry has competed on price due to a high degree of standardization of services and low switching costs for consumers. Through technology and network effects, Kollect has the potential to be very competitive on price. Furthermore, the company could differentiate itself from competitors through its brand, excellent service and new technology (such as the commercial app). By differentiation, Kollect can increase switching costs and by making its services unique, the company can charge a higher price.

As Kollect has a first mover advantage, the company has the opportunity to leverage its market position and establish itself as the leading marketplace within waste management. From such a market position, Kollect would be able to create significant durable competitive advantages through network effects and its brand.

Valuation

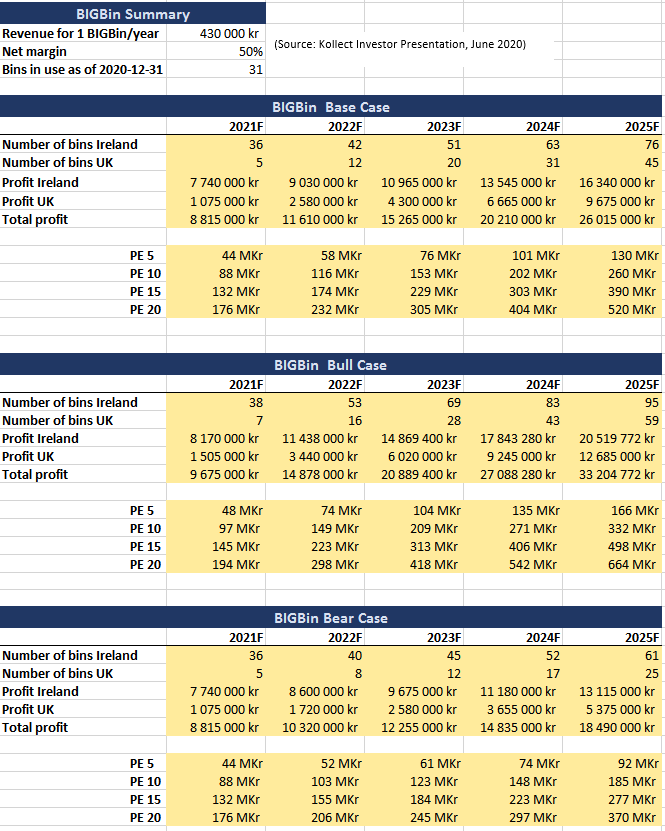

When looking at the numbers and valuation, I decided to separate the two business areas and make individual projections for them. See pictures:

I would say that the assumptions about growth in the number of bins, especially a few years out, could prove to be quite conservative. With additional financing the company should be able put out significantly more bins as capital has been the main constraining factor so far. The company has already been provided with financing to open an additional 10 BIGBins during 2021. Existing BIGBin-partners like Circle-K could also want to roll out the BIGBins on a nationwide scale. The contract with Circle-K covers potential use of the BIGBins at 160 different Circle-K stations as well as an additional 260 sites from the Circle-K dealer network.

There is a huge demand for a solution like the BIGBin all across Europe. However, capital is a constraining factor. A way for Kollect to scale this business area would be to license out the BIGBin concept or that the company partners up with companies to provide more bins in new geographies. My calculation excludes this optionality.

Here are my calculations for the marketplace that Kollect operates:

In the case of Kollect, the GMV is equal to gross revenue as Kollect takes the orders from the customer and then sub-contracts the fulfilment to suppliers. Gross revenue also includes the revenue from the BIGBin business. The cost of sales is the amount that Kollect pays out the suppliers to fulfill the placed orders. This information has been confirmed by the IR team.

The take rate is a key variable to monitor. If Kollect is able to solidify their position in the market they could get pricing power and be able to charge a higher take rate. The additional cost could either be taken by the end consumer or the waste contractor (or by both).

This calculation does not take into account the revenue that other complementary services that the company can and will provide customers in the future. The Centralised Billing service and the mobile app provided to commercial customers are examples of such services. I would also like to note that the waste management industry as a whole is experiencing slight growth (single digit % growth) and thus the total TAM for Kollect is growing.

When looking at the valuation of the company, peer valuation is also a very useful toolkit. When conducting peer valuation, the company could be compared to other online marketplaces such as Jumia Technologies, CDON and eBay. As Kollect has 61 % recurring revenues, it could also be compared to SaaS stocks such as Fortnox, Carasent and 24SevenOffice. I believe that other marketplaces are more suitable peers however.

Kollect trades below peer valuation even though it is a rapidly growing business with improving margins and a scalable business model. Marketplaces:

SaaS companies:

So how much is the company worth? To be entirely honest with you, I have no idea. I am, however, reminded of a quote that has been attributed to Benjamin Graham: “You don't need to know a man's weight to know that he's fat”. The company is growing extremely fast and margin improvements are continuously made and it is very likely that the company will be breakeven or profitable in the near future. Mangold estimates that the company will become profitable in 2021 and this would make the company far less risky and this would likely be reflected in the stock price. I believe that the company has a long runway and that shares can be bought at a reasonable price.

Risks

In my view, the main risk for the company is the liquidity risk. The company currently operates at a loss and external financing is thus needed to cover expenses. However, I believe management is quite cost-focused as they showed prudence and efficiency in cutting costs during the Covid-19 outbreak. During this period, management drastically decreased spending in order to safeguard the company from liquidity risk.

During the later part of 2020, the company announced the distribution of warrants of series TO1 to provide the company with additional financing. The exercise period to subscribe for new shares with warrants from series TO1 will be from August 9 to August 20, 2021.

“A total of 3,692,805 warrants of series TO1 will be issued, of which 900,000 will be issued to investors in the directed issue, 300,000 to the lender and 2,492,805 issued to current shareholders in the Company.”

“Warrants of series TO1 will, upon full exercise, give the Company the opportunity to raise up to a maximum of approximately SEK 55.4 million, depending on the subscription price. Upon full exercise of the warrants of series TO1, the dilution will amount to approximately 38.6 percent, in proportion to the number of shares after the registration of the directed issue.”

A warning sign and definitely something to be aware of is that all three founders, Mr Connor, Mr Hegarty and Mr Skuse have all sold some of their TO1 Warrants. I can only speculate why they chose to do this. They may believe they already have a large enough stake in the company or feel that their private finances do not allow them to exercise the warrants. On a call regarding the warrant programme, Mr Connor claimed that he and the other founders sold warrants as their personal finances do not allow them to exercise the warrants. Management voiced that they intended to minimize the lapse rate of the warrants and they aim to raise as much financing as possible through the warrant programme. While the founders have sold warrants, they have not sold any shares since the company went public.

Kollect works in markets where waste management is largely privatized. If large regulatory changes affecting the privatization of the market would occur, this would negatively affect the company. This is not beyond the realms of possibility as the regulation and privatization of the waste industry looks quite different in other countries than in Ireland and the UK. In Sweden for example, waste is handled by municipalities instead of waste companies. On the other hand, deregulation and more privatization of the industry would be positive for the company.

Ending thoughts and possible catalysts

The company is undoubtedly a nano cap as the company has a market cap of around 80 MSEK. I believe the company is flying under the radar as investors have not realized the strong unit economics and competitive advantages of the business.

The following text is the company description on Avanza, one of the largest online brokers in Sweden:“Kollect on Demand Holding is active in the energy sector. The company specializes in the development of waste management. The business runs via several business areas with a focus on waste collection and delivery. Handling is carried out of, for example, household waste, commercial waste, and the removal of bulky rubbish. The largest business is found in the European market.” (Text has been translated from Swedish to English).

This description does not describe the exciting business model that the company has through its online marketplace, but rather, describes Kollect as a traditional waste contractor. The investor collective is therefore, understandably, put off by the description and thus remain unaware of the company’s operations and future prospects. However, this of course creates an information advantage to investors willing to dig in and do the work of analyzing the company.

Even though the exercising of warrants will result in significant dilution, I believe that the capital raise will take a major risk off the company. With growth capital, the company will be able to ramp up their operations to meet the demand that is already there and waiting for their services. While investors will be diluted, they will now be shareholders of a less risky corporation with capital to fund future growth. Furthermore, equity financing is preferable to debt financing as the company does not generate a positive cash flow. Ultimately, this capital allows for greater investment in the business which will spur growth and ultimately, this will in my opinion make Kollect a more attractive investment.

The closing of commercial businesses such as restaurants, building sites and hotels in Ireland due to the pandemic has negatively affected Kollect. The commercial business segment delivers higher margins for Kollect but despite the shutdowns during 2020, Kollect was able to significantly grow. The reopening of Ireland and the UK is thus a positive near term headwind for the company, especially because Kollect has launched specialized services, such as centralized billing, for these customers. It is also quite likely that there is some pent up demand for construction, hotels and other activities which could increase waste collection needs. I believe the market underestimates the effect that the reopening of the economy will have on the company and this could be a catalyst for the stock.

A catalyst in small caps can often be that institutional investors take an interest and start to build a position. As of now, institutional ownership is basically nonexistent in Kollect. One major reason for that is that most funds have mandates that do not allow them to invest in nano caps such as Kollect. However, I believe there could be significant institutional interest in the future. Not only does the company have an attractive business. but also a strong ESG profile. Kollect increases transparency and the focus on sustainability in waste management which is an industry that affects people's health and CO2-emissions. In time, the company could see significant interest from investment funds with a focus on sustainability. If the company is able to deliver operationally and grow bigger, funds would be within their mandates and would be able to buy shares. This could serve as a catalyst.

As the company is a first mover in innovating and digitizing the waste management space, Kollect has potential of becoming the top of mind company for people looking to get rid of waste. Traditional waste contractors are geographically restricted and very local whereas Kollect’s marketplace has no such built-in geographic restriction. Therefore, the company has a far wider reach than any other traditional waste company could ever have. It is very hard to see how individual waste contractors alone could be able to compete with the offering that Kollect is able to provide today (and in the future as the service improves). If successful in establishing itself in the market, Kollect will be able to create strong, durable economic moats through technology and network effects - in an industry that already faces structural barriers to entry.

Comments

Post a Comment